Whether to buy a house or rent one? This is one of the biggest dilemmas working professional face in India. The question is especially true in the post-pandemic environment where homes have become our place of work as well. The work from home or WFH has suddenly increased our affinity to home unlike in the past when homes were just a place to get rest after a hard day at work. This was especially true in big cities like Mumbai, Delhi and Bangalore where professionals would be out on the streets or in their offices for 12-14 hours at a stretch.

WFH has also forced many professionals to reassess the utility of their current residence and many found them to be less-than-ideal for the post-Coronavirus world.

Not surprisingly, many people are now actively looking for new homes that will better fit the new work-life balance and also provide enough breathing space to their family members.

This brings us back to the original question – should you buy a new house or rent-in a more spacious property in a better locality? Buying a house is most often the biggest financial decision any of us will ever make. So, before you take a plunge and sign on the dotted lines let’s break down the pros and cons of the decision.

1. Buying a house means a large committed monthly expense for the next 20 years or even 30 years. This means living with a loan for most of your working life. This will require a fair bit of financial discipline and motivation and not to mention sacrifices in the initial years.

In contrast, rental expenses are lower and can be flexible, especially in the era of work from home. You can negotiate the rents down or choose to change the house or locality if it becomes unaffordable.

2. The interest on home loans has come down sharply in the last one year, which has translated into lower equated monthly instalment (EMI) for home loans. Till a few years ago, EMI on home loans worked out to be around Rs1000 per month for evert Rs1 lakh worth of loan with tenure of 20 years. Now, this has declined to anywhere between Rs 750-800 per month. This has made homes affordable, especially for those who escaped COVID-19 with minimal or no loss in their salary or income.

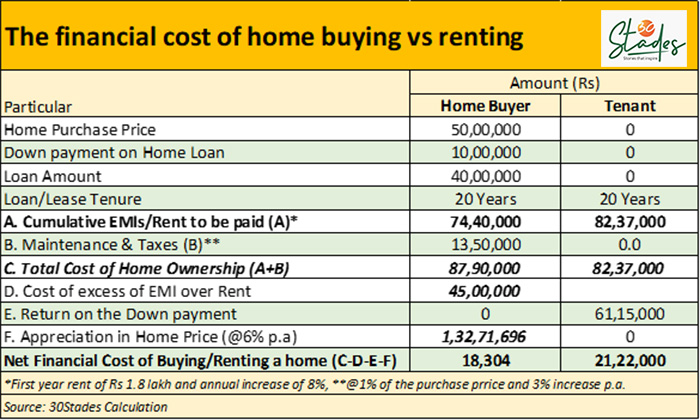

3. Home purchase also requires you to pay margin money or make a down payment to avail the loans. Most banks ask for a 20 percent down payment amount as the borrowers’ equity contribution towards the house, though margin money can be reduced to as low as 5 percent for some borrowers. The higher the amount of down payment, the lesser is your EMI outgo. A house worth Rs50 lakh will require you to make a down payment of around Rs10 lakh. This means that you need to start saving a few years prior to your decision to buy a house or dip into your retirement corpus such as a provident fund or take help from your family or do a mix of all.

4. As a home-owner you will also need to spend money on maintenance and property taxes and occasional repairs and refurbishments. While the maintenance cost is levied by the housing society that provides the common facility, property taxes are charged by the municipal bodies. At the prevailing rate, running expense could be anywhere from 1-2 percent of the property acquisition cost depending on the amenities and the apartment size. Expect these expenses to rise at an annual rate of 3-4 percent in line with the cost of living.

5. A tenant on the other hand just has to bother about the monthly expenses and leave all other worries to her landlord. Besides, rents are still much lower than EMIs for apartments in most cities. For example, at the current home loan interest rate of around 7 percent, a house worth Rs50 lakh will need around Rs31,000 as EMI assuming a down payment of 20 percent. In comparison, the same apartment can be a monthly rent of around Rs 15,000. However, unlike EMI which is largely fixed during the tenure of the loan, the rents are expected to grow at 8-10 percent every year.

6. As a tenant, you also have the option to invest the potential down payment of the margin money into high yielding assets such as equity mutual funds, corporate deposits or provident fund. An initial investment of Rs 0 lakh into diversified equity mutual fund will grow to a corpus of around R 61 lakh at the end of 20 years assuming an annual return of 10 per cent. In the last five years, diversified equity mutual funds have given 11 per cent annualised returns on average. This is an opportunity loss for home buyers that they can hope to recover through the appreciation in their home price over the years.

Also Read: Lessons from COVID-19 Lockdown: 10 tips to build your emergency fund

7. Now let’s compare the full financial cost of home ownership with that of a similar home on rent over a 20-year period.

As the above calculation shows, renting an apartment is cheaper if we only look at the out of pocket expenses and tenant is smart and disciplined enough to invest the equivalent amount of margin money in well-managed equity mutual fund. But buying a house becomes financially rewarding if it appreciates in value over time.

Assuming home prices rise at an annualised rate of 6 per cent, the house price will triple in value over 20 years and your initial Rs10 lakh equity investment in the house will appreciate by around Rs1.32 crore.

8. So, when you decide to purchase a home rather than take it on rent, you have decided to live a frugal and less lavish lifestyle. Home ownership forces you to raise your savings directly or indirectly and forces you to take a hair-cut in your discretionary spending and lifestyle such as exotic holidays, expensive cars, jewellery or even luxury clothing. This makes home ownership a lifestyle issue for many who like to explore the world. The above calculations should help you decide clearly.

(Karan Deo Sharma is a Mumbai-based finance and equity markets specialist).

(This article is in arrangement with 30Stades.com)