Imagine being stuck in a situation where you have just been diagnosed with a critical life altering illness – a heart condition, cancer or a kidney failure. Are you or your family prepared to face the financial consequences? Often we push away such thoughts, convincing ourselves that it would not happen to us.

But we live in a country where one is 10 times more likely to die of a heart disease compared to people in other countries, as per a report by Indian Heart Association. The report also mentioned that of all the heart attacks in India, half occur in people under 50 years of age and 25% of them to those under 40 years of age.

While heart ailments is just one of the many illnesses that a critical insurance policy covers, it is very important to start early, and not after getting diagnosed of an illness.

This would not only affect the premiums, but in extreme cases make you unfit for availing a critical illness cover.

What is a critical illness cover in life insurance policy?

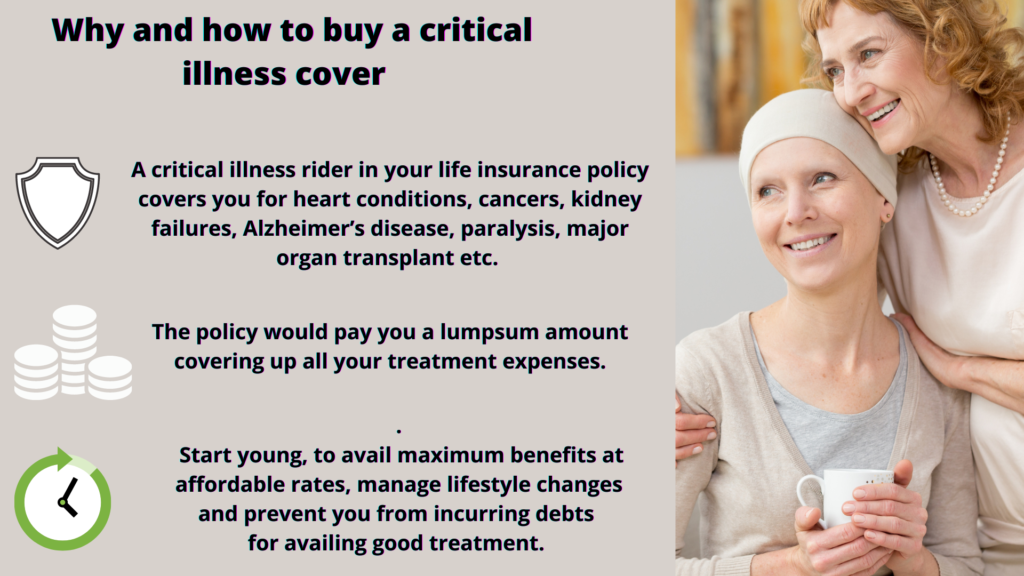

A critical illness rider in your life insurance policy covers you for illnesses that are not only life threatening, but are also capable of altering your lifestyle – like a stroke or paralysis where you are unable to be employed for prolonged periods of time.

If you have a critical illness rider, the policy would pay you a lumpsum amount that you have opted for, covering up all your treatment expenses.

Having a critical illness policy thus helps you to be prepared for any such exigency while also preventing you the mental agony of your finances drying up or even incurring debt for meeting the mammoth treatment costs.

What ailments it covers?

This is a question that you should look into while considering the various life insurance covers available in the market. The number of critical illnesses that a plan covers varies from insurer to insurer and ranges from 30 to 60 illnesses.

These include heart conditions, cancers, kidney failures, Alzheimer’s disease, paralysis, major organ transplant etc.

Check with your insurer on the covers being offered and opt for a plan which you feel is the most comprehensive for you.

Can you buy a cover after being diagnosed with a critical illness?

As per Suresh Agarwal, Chief Distribution Officer, Kotak Life Insurance, prolonged illness can be classified into broadly two types: Critical /Terminal Illness – e.g. cancer, cardiac conditions etc., and lifestyle illnesses, which can be controlled or managed like diabetes and hypertension.

As per Agarwal, for the first category of illnesses, if they are pre-existing, it could be difficult for the individual to buy a life insurance plan. Under some circumstances, the cover could still be offered at a rated-up premium. For example if cancer is now in remission etc., but these are case-to-case decisions.

For the second category, the individual can get life insurance cover at a slightly higher premium (or no increase if is marginal or very nascent levels) than the normal rates.

Once policy is issued, the premium would stay constant throughout the tenure of the policy.

Agarwal also added that it was very important for the policyholder to disclose all details upfront in order to ensure there is no issue for the family/nominee in the event of a claim.

So does a pre-existing condition like diabetes, high blood pressure has impact on your critical illness policy too? Yes. Given the intensity of your pre-existing condition, your critical illness policy premiums will get affected.

Atri Chakraborty, Chief Operating Officer at IndiaFirst Life Insurance Company, says life insurance companies use algorithms and data to decide, based on your health history, hobbies, and other personal details, how good a risk it is to insure you for critical illness cover.

Atri gave an example where someone having diabetes wants to avail a cover then depending on the present condition, duration of illness, treatment regimen and other personal details, the person may get a cover wherein premiums could be at least 25 percent to 30 percent higher than that for a healthy person.

Conclusions:

- A critical illness plan pays you a lumpsum in case you are diagnosed with any of the listed medical conditions. This lumpsum amount can help you pay up the treatment expenses, manage lifestyle changes and prevent you from incurring debts for availing good treatment.

- The critical illness benefit is best opted when you are healthy. Start young, to avail maximum benefits at affordable rates.

- If you have some pre-existing conditions, you may still opt for a critical illness cover, while keeping the insurance provider informed of your medical history. The premiums and coverage may vary from insurer to insurer; choose a cover that best suits your needs.

(Elizabeth Mathai is a Kochi-based content creator and a therapist, with expertise in insurance)